What You Need To Know About Homeowner’s Insurance

Homeowner’s insurance is a must-have to protect what’s probably your biggest investment – your home. And while you never want to think about worst-case scenarios, the right coverage is basically your safety net if something goes wrong. Here’s how it helps you.

In the simplest sense, it gives you peace of mind. Knowing you have protection against unexpected events helps you worry less. And with such a big purchase, having that reassurance is a big deal.

And while your first insurance payment will be wrapped into your closing costs, you’ll want this to be a part of your budget beyond closing day too. That’s because it's a recurring expense you’ll have once you get the keys to your home.

Here’s what you need to know to help you budget for this important part of homeownership today.

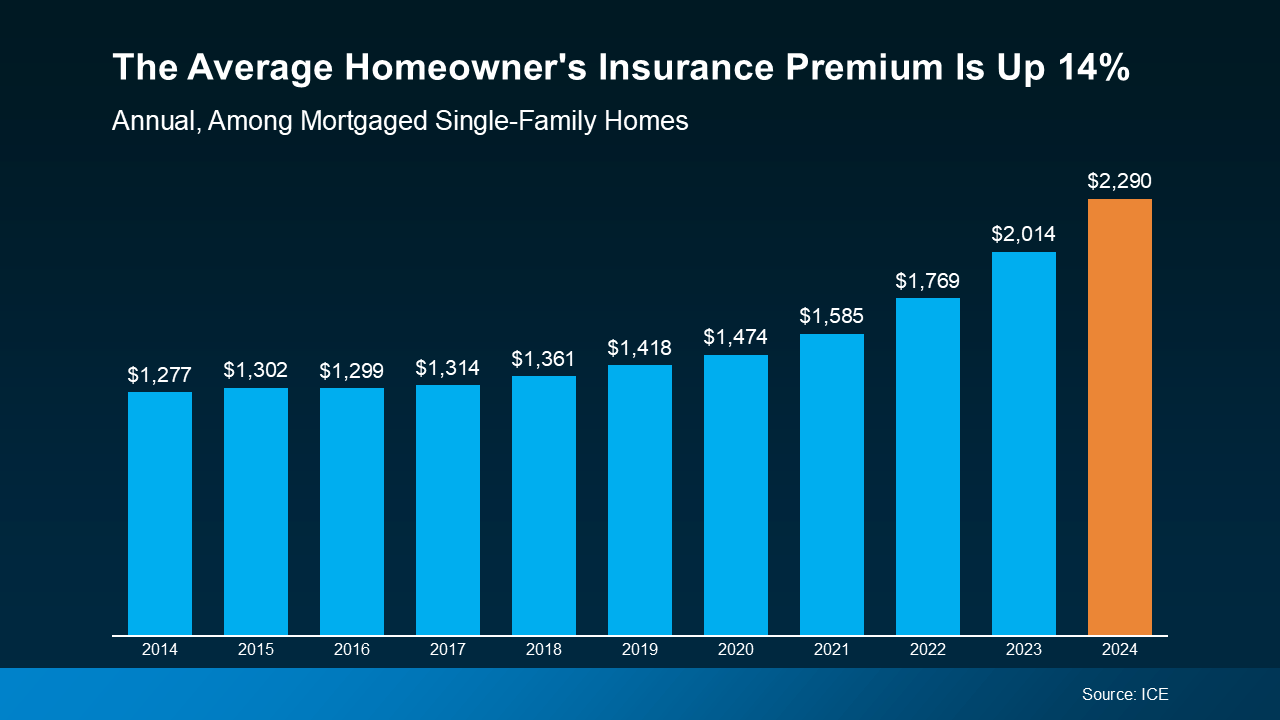

In recent years, insurance costs have been climbing. According to Insurance.com, there are four big reasons behind the jump in premiums:

Basically, disasters are happening more often, repairs cost more, and insurers have to adjust their rates to keep up. Data from ICE Mortgage Technology helps paint the picture of how the average yearly premium has climbed over the last decade (see graph below):

Homeowner’s insurance is a must to protect your home and your investment. But with costs rising, you’ll want to do your homework to balance the best coverage you can get at the best price possible.

Homeowner’s insurance rates vary widely based on location, provider, and coverage. Shop around and compare quotes before settling on a policy. And don’t forget to ask about discounts. Things like security systems or bundling with auto insurance could help lower your insurance costs.

When you’re planning to buy a home, it’s important to look beyond just your mortgage payment. You’ll also want to budget for your homeowner’s insurance policy. It gives you a lot of protection against the unexpected. And while it’s true those costs are rising, there are things you can do to try to get the best price possible.

What’s your biggest concern when it comes to budgeting for homeownership? Let’s talk through it and make sure you’re set up for success.

Stay up to date on the latest real estate trends.

February brought extraordinary price appreciation to San Francisco, with both single-family homes and condos posting impressive year-over-year gains. Single-family hom… Read more

Single-family home prices in Alameda County bounced back to $1.3 million, while condo prices remain mixed with a notable rebound in Contra Costa County.

Interview with Eddie O'Sullivan, Founder/Realtor of Elevation Real Estate

Single-family home prices surged by more than 16% year-over-year, marking one of the strongest January performances in recent memory.

Single-family home prices posted modest year-over-year gains across both counties, while the condo market continued to slide with double-digit declines in Contra Costa… Read more

The San Francisco housing market closed out 2025 with impressive year-over-year gains in median sale prices. Single-family homes saw an 8.63% increase, with the median… Read more

As we moved through the holiday season, inventory levels dropped significantly across the East Bay.

The single-family home market is on fire in San Francisco right now, as the median sale price for a single-family home is reaching the highest level it’s reached in th… Read more

It’ll be important to pay attention to how this market evolves over the seasonally slow winter months, as dwindling inventories might drive prices up over time.

You’ve got questions and we can’t wait to answer them.