San Francisco Market Update - March 2023

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Stay up to date on the latest real estate trends.

David's East Bay experience, creativity, and dedication to his clients made him a perfect fit for Elevation Real Estate

San Francisco's single-family home market continues to reach new heights, with the median sale price climbing 22.56% year-over-year to $2,200,000. This marks one of th… Read more

Prices are on the rise across the board, with single-family homes and condos both posting year-over-year gains for the first time in over a year.

Median sale prices continue their remarkable ascent, with single-family homes up more than 21% and condos up more than 18% year-over-year.

After several months of relative stability, single-family home prices in the East Bay showed some softening in April.

May 9th | 10AM - 1PM | 4 Norwich Street, San Francisco

Median sale prices are soaring in San Francisco, with condos up more than 27% and single-family homes up more than 18% year-over-year. Inventory levels remain more tha… Read more

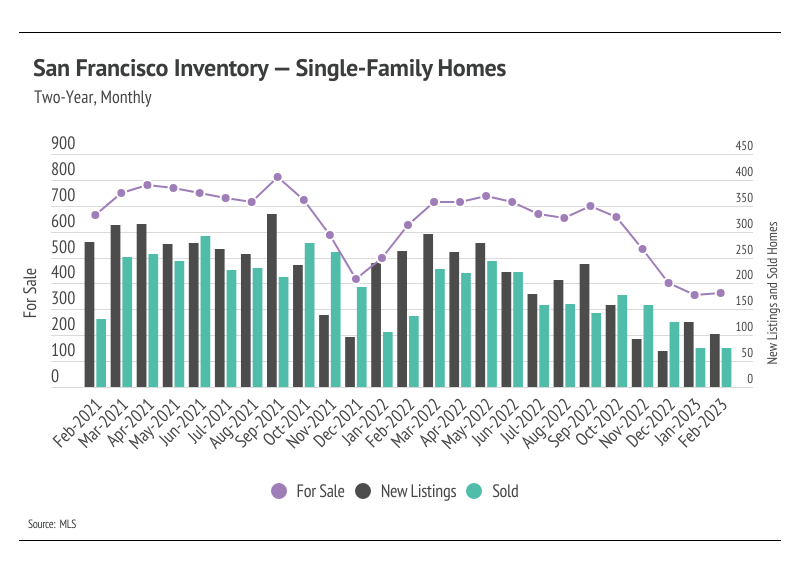

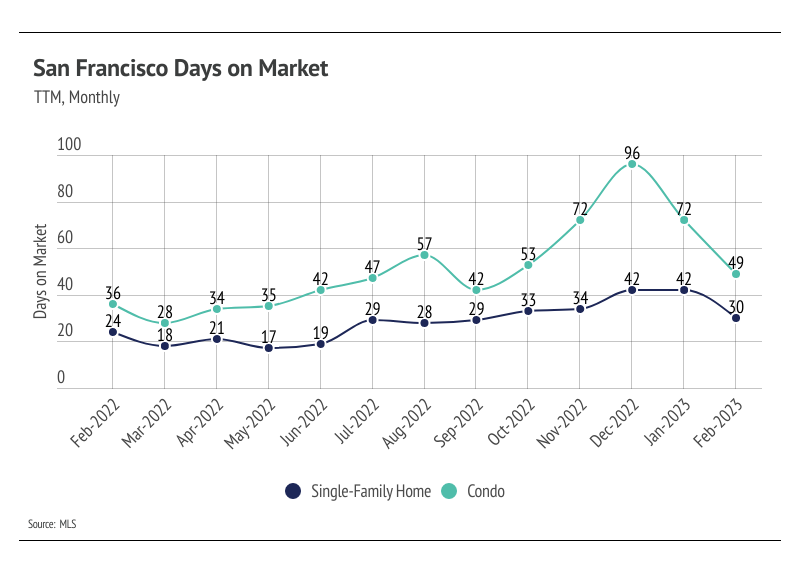

Single-family homes are selling at a blistering pace, with the average listing moving in under two weeks.

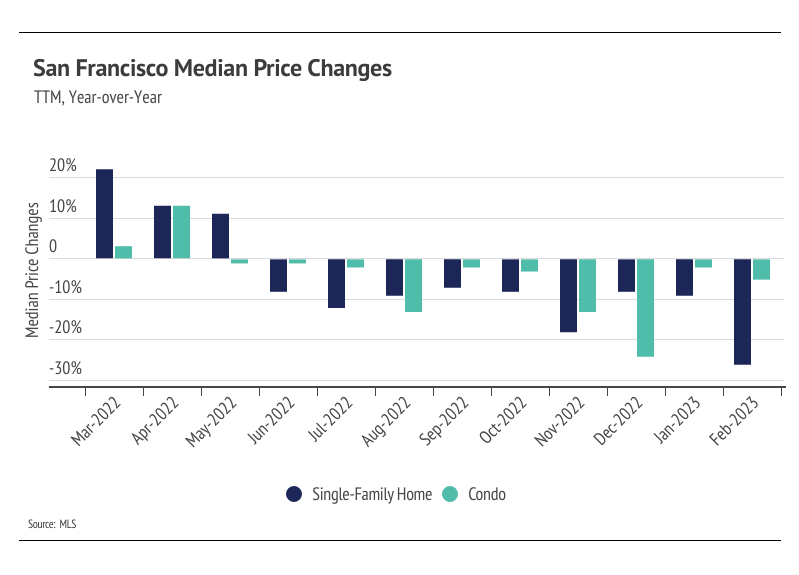

February brought extraordinary price appreciation to San Francisco, with both single-family homes and condos posting impressive year-over-year gains. Single-family hom… Read more

You’ve got questions and we can’t wait to answer them.