3 Key Factors Affecting Home Affordability

Over the past year, a lot of people have been talking about housing affordability and how tight it’s gotten. But just recently, there’s been a little bit of relief on that front. Mortgage rates have gone down since their most recent peak in October. But there’s more to being able to afford a home than just mortgage rates.

To really understand home affordability, you need to look at the combination of three important factors: mortgage rates, home prices, and wages. Let’s dive into the latest data on each one to see why affordability is improving.

Mortgage rates have come down in recent months. And looking forward, most experts expect them to decline further over the course of the year. Jiayi Xu, an economist at Realtor.com, explains:

“While there could be some fluctuations in the path forward … the general expectation is that mortgage rates will continue to trend downward, as long as the economy continues to see progress on inflation.”

And even a small change in mortgage rates can have a big impact on your purchasing power, making it easier for you to afford the home you want by reducing your monthly mortgage payment.

The second important factor is home prices. After going up at a relatively normal pace last year, they’re expected to continue rising moderately in 2024. That’s because even with inventory projected to grow slightly this year, there still aren’t enough homes for sale for all the people who want to buy them. According to Lisa Sturtevant, Chief Economist at Bright MLS:

“More inventory will be generally offset by more buyers in the market. As a result, it is expected that, overall, the median home price in the U.S. will grow modestly . . .”

That’s great news for you because it means prices aren’t likely to skyrocket like they did during the pandemic. But it also means it’ll probably cost you more to wait. So, if you’re ready, willing, and able to buy, and you can find the right home, purchasing before more buyers enter the market and prices rise further might be in your best interest.

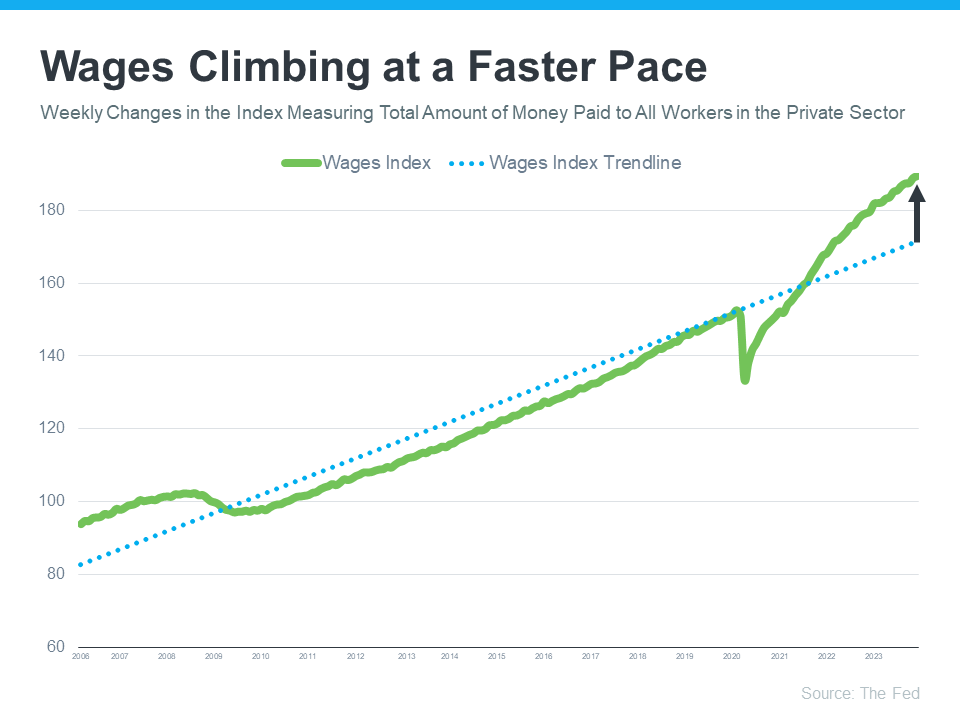

Another positive factor in affordability right now is rising income. The graph below uses data from the Federal Reserve to show how wages have grown over time:

If you look at the blue dotted trendline, you can see the rate at which wages typically rise. But on the right side of the graph, wages are above the trend line today, meaning they’re going up at a higher rate than normal.

Higher wages improve affordability because they reduce the percentage of your income it takes to pay your mortgage. That’s because you don’t have to put as much of your paycheck toward your monthly housing cost.

Home affordability depends on three things: mortgage rates, home prices, and wages. The good news is, they’re moving in a positive direction for buyers overall.

If you're thinking about buying a home, it's important to know the main factors impacting affordability are improving. To get the latest updates on each, let's connect.

Stay up to date on the latest real estate trends.

David's East Bay experience, creativity, and dedication to his clients made him a perfect fit for Elevation Real Estate

San Francisco's single-family home market continues to reach new heights, with the median sale price climbing 22.56% year-over-year to $2,200,000. This marks one of th… Read more

Prices are on the rise across the board, with single-family homes and condos both posting year-over-year gains for the first time in over a year.

Median sale prices continue their remarkable ascent, with single-family homes up more than 21% and condos up more than 18% year-over-year.

After several months of relative stability, single-family home prices in the East Bay showed some softening in April.

May 9th | 10AM - 1PM | 4 Norwich Street, San Francisco

Median sale prices are soaring in San Francisco, with condos up more than 27% and single-family homes up more than 18% year-over-year. Inventory levels remain more tha… Read more

Single-family homes are selling at a blistering pace, with the average listing moving in under two weeks.

February brought extraordinary price appreciation to San Francisco, with both single-family homes and condos posting impressive year-over-year gains. Single-family hom… Read more

You’ve got questions and we can’t wait to answer them.